MOBILITY BIOMETRICS

If someone told us a decade ago, how mobility is going to make sweeping changes in every aspect of our life, we would have scoffed at the very idea. But look at us today, mobile phone and technology have become an integral part of our life, from e-commerce to checkout lanes at supermarkets, no sector has been left untouched by the innovation in mobile technology.

Lending institutions have joined the race of mobilising the sector, due to the demand of the “smartphone obsessed” clients of today. Leveraging the ground-breaking capabilities of the next-gen mobile phones have helped them to streamline their workflows and reduce their overall turnaround times.

Loan Origination

Process

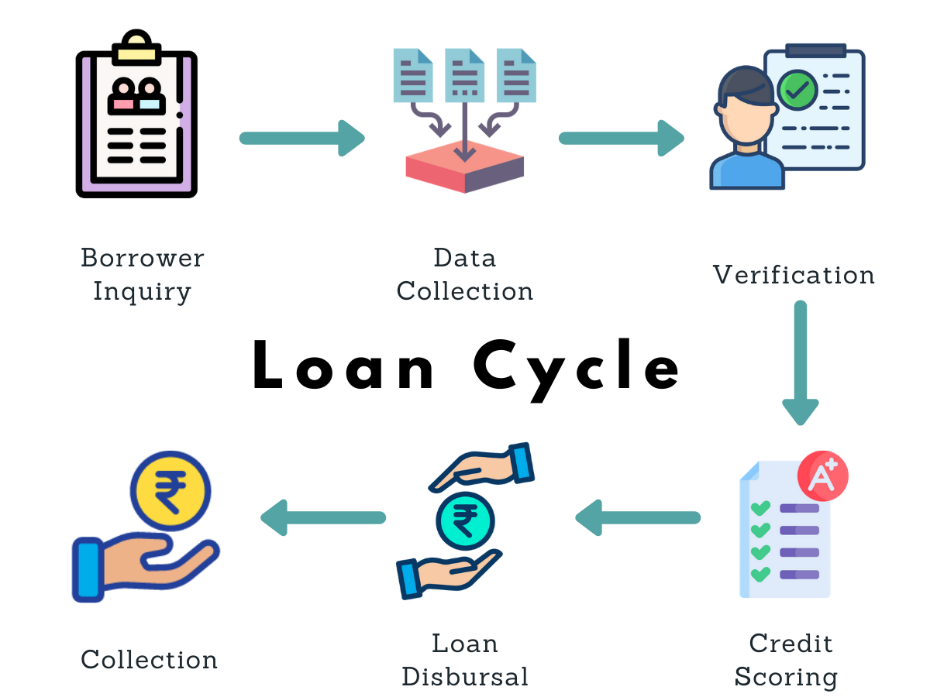

Traditional loan origination process used to be a nightmare of arduous paperwork. Once a potential borrower is identified, a sales agent / Business Correspondent contacts them to complete the application paperwork and to gather documents for underwriting. The sales agent would then submit the application, which would be forwarded to the loan officer subsequently.

In the case of incomplete documentation, the sales agent may have to get in touch with the borrower and retrieve them. Else, the application would be rejected. As you could see, a small oversight could have an adverse effect on the turn-around-time.

Once the application is submitted, it may take quite a few days to complete the verification process. Even retrieving the application status amidst this chaos would be highly impossible, which would just aggravate the already concerned borrower.

Mobility in Loan Origination

The new-age mobile applications not only eliminate the application paperwork but also take care of documentation and credit assessments injecting a sense of transparency into the process.

e-KYC

Mobile apps have integrated e-KYC solution; this aspect simplifies the onboarding process, reduces the mayhem of submitting relevant proofs (address proof, identity proof, pan card, etc. and) completes the entire verification process in a few seconds.

However, not everyone would be allowed to access the confidential data of an individual, and it could be done only with the proper consent of that person.

In the case of Aadhaar, the verification process could be carried out using different methods, biometric verification, OTP & offline.

Overall Impact

Mobility loan origination helps lenders Sales Agents.

Empowered with a mobile application, sales agents could complete the entire application process within a matter of minutes. All they would have to do is fill up a form of borrower’s information, upload required documents and submit it online.

As the entire process is completely automated, there would be no room for error or incomplete documentation. A sales agent could easily retrieve information about the status of an application through the mobile device and alleviate the concerns of a customer immediately.

Customers

Instead of depending on a Banking Consultant, customers could use the self-service mobile app directly and apply for loans right from the comfort of their home.

The user-friendly nature of mobile apps would help them complete the application soon and keep them informed of the status of their loan application.

Financial Institutions

The automated application process and the document identification aspects available in a sales agent’s mobile app reduce manual labour, simplify the loan origination process, and improve customer satisfaction.

It accelerates the lending process, eliminates paperwork, reduces latency, makes the application status transparent and keeps customers satisfied.

Repayment/Collection

Collection is an integral part of the lifecycle of a loan. Any delinquency in this stage could cause problems for both parties involved – Financial Institutions and Borrower.

Technology has made the tedious process a breeze. We are aware that tech savvy customers could make their repayment with the touch of a screen using their mobile app, but what about technically challenged folks who are in remote areas of the nation?

This is where a Banking/Business Correspondent comes in. They bridge the gap between financial institutions and their customers.

BCs act as representatives of the lenders and play a substantial role by taking care of all crucial tasks like collecting loan applications from villagers, forwarding them to the financial institution, field investigation, and also helping the financial institutions in collecting EMIs/recovering the loan money.

Equipped with a mobile device and Biometric device that is integrated with the core banking cloud application, a BC could perform transactions on behalf of a customer seamlessly. Instead of hustling around with collection sheets they could just update the repayment status on their mobile app immediately.

Besides replacing the collection sheet, a mobile app could also act as a knowledge base for loan officers, which they could refer to answer customer queries about repayment schedule, previous payments, pending balance, etc.

Though it seems great as a business model, it has its fair share of risks as this somewhat transfers the overall responsibility to a third party. Regulation measures like rigorous internal audits and policies can mitigate the risk factor only to a certain level.

To ensure that compliance is maintained, constant supervision of the third-party agents becomes fundamental. Mobility comes in handy to resolve this issue as well. The built-in GPS tracker in the mobile app would help the lenders keep track of a field agent’s real-time location and prevent any potential frauds.

In short, mobility could speed up the repayment process considerably, enhance the operational efficiency of a collection officer, and prevent potential frauds (like the EMIs being used as Float Money).

Notifications

Right from the stage of application to fulfilment and repayment, mobility solutions tend to come in handy with the frequent notifications about the loan status or critical reminders regarding the loan account.

Customers get push notifications about a change in their loan status or reminder about repayment schedule on their app. Field officers get notifications about the allocation of a case or the loan account on their mobile device

Summary

Mobility has unarguably played a huge role in reducing the inefficiencies in the lending sector. The latent process of traditional loans has been transformed completely to a swift mode using the latest technological advances.

Mobility reduces the overall TAT of a loan application process, injects transparency into the equation, reduces staff problems, promotes user experience, and bridges the gap between customers & financial agency with just a touch of a screen.

Undoubtedly, Mobility is the way forward for rapid development in the lending sector. As the Mobile phones have become an integral part of an individual’s life, the mobility solutions have turned out to be a “must-have” feature for Financial Companies to gain traction in the lending industry.

Precision’s unique InnaITTM SDKs, framework and certified UID biometric devices can come in of use while implementing the eKYC solution described above.

The attributions for the blog are:

- How Mobility is transforming the Lending Sector, Finextra.com

- About eKYC paperless, uidai.gov.in

- How Mobility Is Transforming the Lending Sector, habiletechnologies.com